stock")

williams sonoma company WSM benefits from a solid operating model, e-commerce business and B2B initiatives. Its focus on digital initiatives and global expansion plans bodes well. The company is expanding globally, with a particular focus on the Indian market, and the brand's momentum is exceeding expectations.

However, continued macroeconomic uncertainty and global geopolitical tensions are a concern for the company's growth prospects.

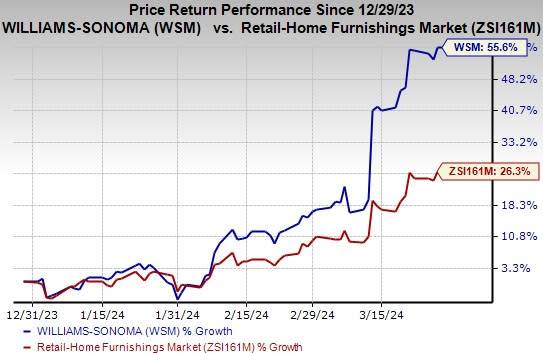

This multichannel specialty retailer of quality home products has grown 55.6% over the past three months compared to the Zacks Retail – Home Furniture industry's growth of 26.3%. Currently carrying a Zacks Rank #3 (Hold), the Zacks Consensus Estimate for fiscal 2025 earnings has increased from $14.69 to $15.37 per share over the past 30 days, solidifying its growth trend.

Image source: Zacks Investment Research

This upward trend is supported by a solid VGM score of A, contributed by a Momentum and Growth score of A, and a Value score of B. This positive trend indicates bullish analyst sentiment, solid fundamentals, and continued near-term outperformance.

Factors driving growth

Focus on e-commerce channels: Williams-Sonoma is one of the largest e-commerce retailers in the United States. Through its innovative efforts, the company has fostered the growth of e-commerce. E-commerce adoption is increasing, driven by in-house technology platforms, rapid experimentation programs, content-rich online experiences, and marketing strategies.

The company is focused on best-in-class retail operations. We continue to enhance the in-store experience with inspiring products and next-level design services. Ongoing retail optimization efforts have transformed vehicles to be placed in the most profitable, exciting and strategic locations.

WSM's capital allocation plan for 2024 prioritizes funding operations and investing in long-term growth. The company plans to spend $225 million in capital expenditures to invest in the long-term growth of the business, with 75% of this investment earmarked for driving e-commerce leadership and supply chain efficiency. Masu.

Digitalization initiatives: On the digital side, WSM maintains tight control over advertising spend, optimizing spend to focus on the most productive channels, while maintaining flexibility to experiment with formats that attract new audiences. As one of the largest e-commerce companies, the company continues to strengthen its unique e-commerce technology stack and positions itself as a leader in the retail industry through its use of AI in its technology capabilities.

During the fourth quarter of fiscal 2023, WSM's Canadian operations continued to see momentum due to its focus on improving the online and retail customer experience. The company's digital efforts in the Canadian market are attracting new customers and driving brand results. WSM is pleased with the early positive response to the recently launched Rejuvenation, Mark and Graham and Williams-Sonoma Home in Canada. India, Mexico and Canada remain key strategic growth markets as WSM expands its omnichannel presence globally.

B2B strategies to drive growth: B2B continues to be one of WSM's key initiatives. B2B operates in his two forms: trade and contract. With 1% year-on-year growth in overall business, the company recorded a 31% increase in contract business in FY2023. This rise was driven by his WSM's strengths in the hospitality and housing sectors. Early traction in developing sectors such as healthcare, gaming and senior housing contributed to the upside. WSM is focused on accelerating its contract business and is showing positive momentum.

Concerns

Williams-Sonoma's results of operations are impacted by higher employment and general expenses, as well as higher occupancy costs. Geopolitical uncertainty is also a concern.

Selling, general and administrative expenses as a percentage of net revenue increased to 26.6% in fiscal 2023 compared to 25.1% in fiscal 2022. This increase can be attributed to the deleveraging of payroll costs through higher performance-based incentive compensation. In fiscal 2023, we will improve compared to fiscal 2022 depending on business performance.

Macroeconomic pressures continue to impact WSM's global business. The company expects macroeconomic uncertainty to continue into 2024. Lower interest rates could stimulate the housing market and shift consumer spending domestically, but the timing remains uncertain. Factors such as elections and global geopolitical tensions contribute to this uncertainty.

key pick

The top stocks in the retail and wholesale sector are discussed below.

Brinker International Co., Ltd. EAT Sports carries a Zacks Rank #1 (Strong Buy). The company's fourth quarter results were an average surprise of 212.7%. EAT's stock price has increased by 36.6% over the past year.You can view See the complete list of today's Zacks #1 Rank stocks here.

EAT's 2024 Zacks Consensus Estimates for revenue and EPS are projecting growth of 4.9% and 30.7%, respectively, from year-ago levels.

Texas Roadhouse Co., Ltd. TXRH carries a Zacks Rank #2 (Buy). The company has recorded an unexpected negative profit of 3.9% for four consecutive quarters. The company's stock price has increased 42.9% over the past year.

The Zacks Consensus Estimates for TXRH's 2024 revenue and EPS suggest growth of 14% and 25.1%, respectively, from year-ago levels.

Shake Shack Co., Ltd. SHAK carries a Zacks Rank #2. The company's fourth quarter results were an average surprise of 92.6%. SHAK stock has increased 93.8% over the past year.

SHAK's 2024 Zacks Consensus Estimates for revenue and EPS are projecting growth of 14.6% and 91.9%, respectively, from year-ago levels.

Want the latest recommendations from Zacks Investment Research? Today you can download 7 Best Stocks for the Next 30 Days.Click to get this free report

Brinker International, Inc. (EAT): Free Stock Analysis Report

Texas Roadhouse, Inc. (TXRH): Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

Shake Shack Inc. (SHAK): Free Stock Price Analysis Report

Click here to read this article on Zacks.com.

Zacks Investment Research